Featured

Table of Contents

There is no federal government financial obligation relief program for credit cards. Debt relief business use services to assist you manage and pay off credit card financial obligation for less than you owe. When you settle credit card financial obligation, you and the credit card business agree on an amount you'll pay, which is less than the total balance you owe.

If you don't have a lump amount to use your lenders (the majority of individuals don't), you may choose to stop making credit card payments and instead set aside cash in a devoted account. If you stop paying your lenders for any reason, expect credit history damage and collection efforts. When you have actually enough saved to provide your lenders, settlements can start.

Insolvency filings are public records and can make it hard to get tasks in particular fields. You also offer up control when you file bankruptcythe court tells you how much you will pay (Chapter 13) or what possessions you must give up (Chapter 7) to please your lenders. Bankruptcy has a major negative influence on your credit rating.

On the professional side, debt settlement could help you get out of debt faster than making minimum payments, because you're paying less than the overall balance. A disadvantage of selecting debt settlement for debt relief is that it's most likely to harm your credit standing. Keep in mind, nevertheless, that if you're already falling behind on your payments, the chances are great you've already seen a negative effect on your credit report.

If you're thinking about charge card debt relief programs, research study your options carefully. Check the services offered, the fees, and online reviews to see what other individuals are saying. Regardless of which debt relief program you choose, the most important thing is doing something about it to get your financial resources and credit back on track.

Qualifying for Federal Debt Assistance in 2026

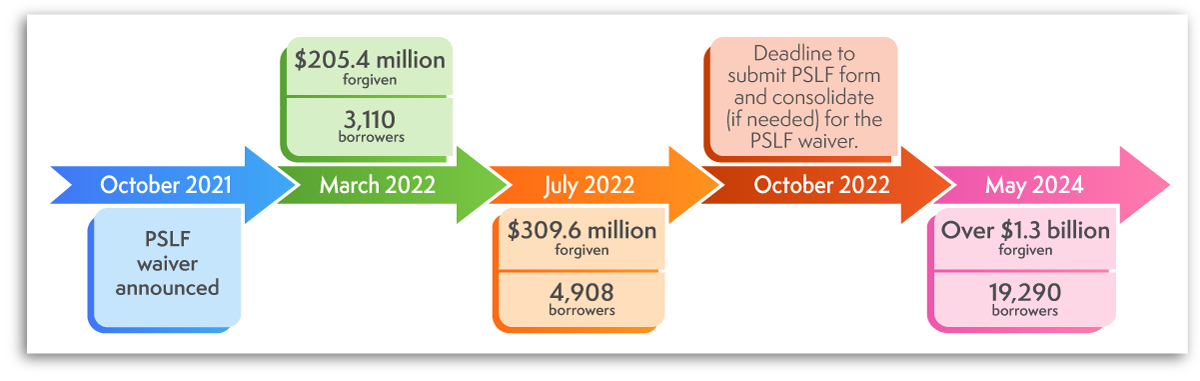

Debtors with federal government trainee loans may qualify for income-driven repayment strategies. They base your month-to-month payments on a portion of your income. This helps make sure you can pay for those payments.

Working long enough in particular public service occupations might qualify you to have the remainder of your financial obligation forgiven. Could paying into an income-driven repayment program for 20 or 25 years.

For example, trainee loan special needs discharge needs proof of your condition. These programs are for individuals in real need, so not everybody will qualify. In many cases, forgiven financial obligation is taxable income. Debt forgiven under federal trainee loan programs is usually an exception. There are a few states where forgiven federal trainee loan debt may be dealt with as gross income.

Trusted Strategies for Handling Personal Debt

Let's attend to some typical misconceptions about federal government financial obligation relief programs to clear up any confusion. Truth: In lots of cases, Internal revenue service and student loan debt forgiveness programs are based on your capability to pay.

Browsing the Emotional Toll of Consistent Financial Obligation CollectionReality: The application process might take some time. There are numerous resources and assistance systems available to help you. Now that we've unmasked these myths, you can better understand what federal government debt relief programs can use.

These programs are developed to assist, not to include more tension. It's worth exploring your alternatives. Federal government financial obligation relief programs don't cover all kinds of financial obligation, however there are other alternatives that can assist. Personal specialists and hardship programs can provide support and solutions. Here's what you can do if you have debt problems the federal government can't fix.

These organizations include private financial obligation relief business and not-for-profit credit therapists. Here are a few of the services they may use: Challenge programs: Numerous financial institutions provide challenge programs to assist you survive bumpy rides. These programs might minimize or pause payments, lower interest rates, or waive charges for individuals experiencing financial trouble.

The Latest Manual to Filing Bankruptcy in 2026

This could result in substantial financial obligation reduction. Credit counseling: A qualified credit therapist can help you create a spending plan and discover money management skills if you register in their debt management program.

Household debt in America is over 18 trillion dollars, according to the Federal Reserve Bank of St Louis. With a lot financial obligation, it's not surprising that lots of Americans desire to be debt-free. If you are searching for debt relief and you desire to say goodbye to your debt for great, take actions to totally free yourself from your lenders in 2026.

Debt is always a financial problem. But it has actually become more challenging for numerous people to manage in the last few years, thanks to increasing rates of interest. Rates have risen in the post-COVID period in response to unpleasant economic conditions, consisting of a surge in inflation triggered by supply chain interruptions and COVID-19 stimulus costs.

While that benchmark rate doesn't straight control interest rates on financial obligation, it affects them by raising or lowering the cost at which banks obtain from each other. Included expenses are typically handed down to clients in the form of greater rate of interest on financial obligation. According to the Federal Reserve Board, for instance, the average interest rate on credit cards is 21.16% since Might 2025.

Comparing Professional Debt Settlement Services in 2026

Card rate of interest might also increase or stay high into 2026 even if the Federal Reserve alters the benchmark rate, due to the fact that of growing lender concerns about increasing defaults. When creditors are scared clients will not pay, they frequently raise rates. Experian likewise reports average rate of interest on car loans struck 11.7% for pre-owned cars and 6.73% for brand-new cars and trucks in March 2025.

Individual loan rates are likewise greater. With numerous sort of debt ending up being more costly, lots of people wish to deal with their debt for goodespecially given the ongoing financial uncertainty around tariffs, and with a recession risk looming that might impact work potential customers. If you hesitate of rates rising or the economy failing, positioning yourself to end up being debt-free ASAP is among the smartest things you can do.

{kind=link}

Latest Posts

Stopping Illegal Agency Harassment Practices in 2026

Qualified Bankruptcy Counseling for 2026 Debtors

How to File for Bankruptcy in 2026